Mortgage Rate Buydown VS Investing

Mortgage Buydown vs. Investing the Difference: A 30-Year Wealth Comparison

When purchasing a $500,000 home in today’s market, buyers are often presented with a key decision:

Should you buy down your mortgage rate… or invest that same money instead?

At first glance, lowering your interest rate feels like the safer, smarter move. But when you stretch the analysis over a full 30-year mortgage term, the math tells a more interesting story.

Let’s break it down.

The Two Strategies

Scenario 1: Mortgage Buydown

-

Loan: $500,000

-

Base Rate: 6%

-

Buydown: Reduce rate (example: down to ~4%)

-

Upfront Cost: ~$25,000

-

Benefit: Lower monthly payment and reduced interest over time

This strategy prioritizes certainty and cash flow.

Scenario 2: No Buydown + Invest the Difference

-

Keep mortgage at 6%

-

Invest the $25,000 instead

-

Assumed return: 7% annually

This strategy prioritizes long-term growth and compounding.

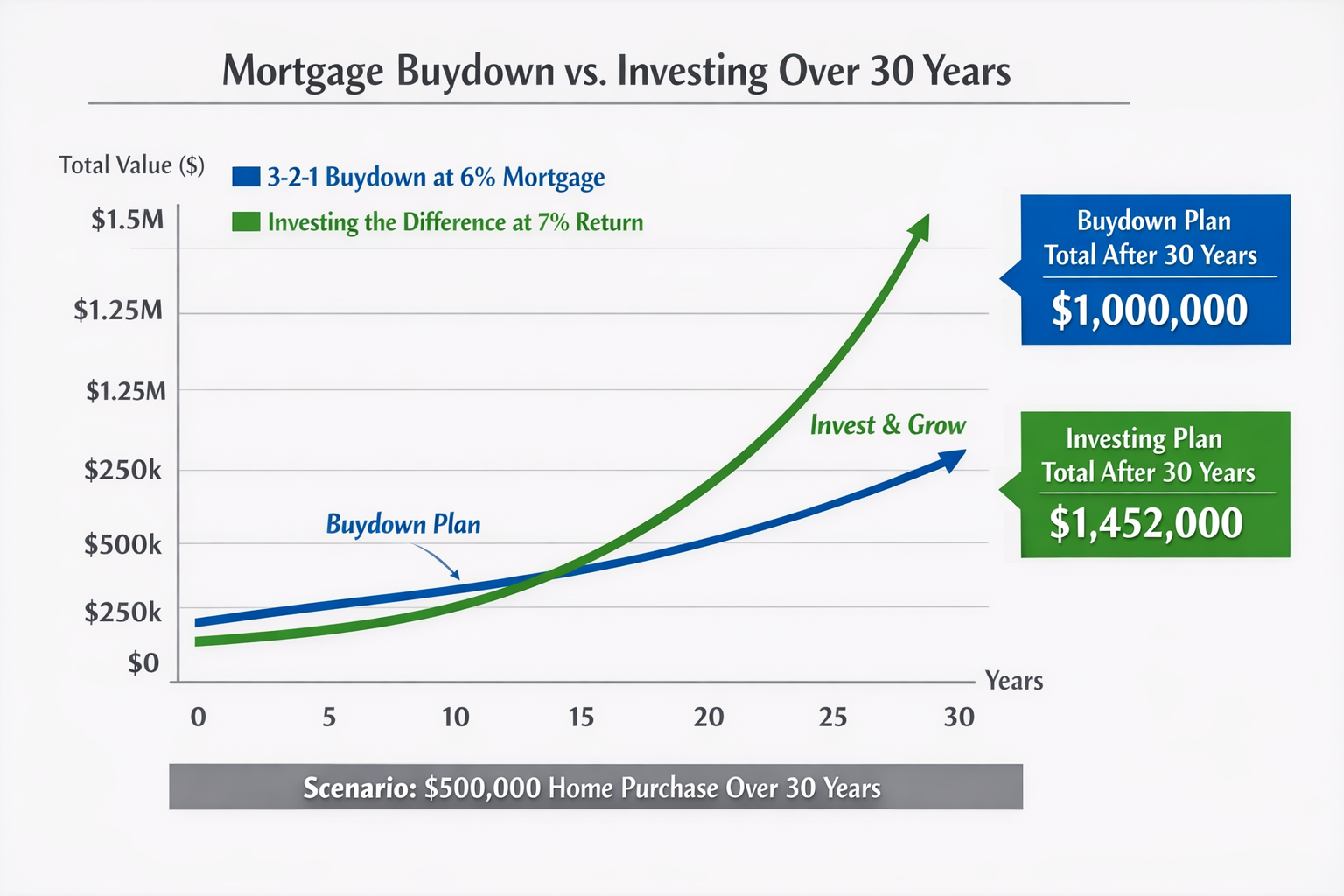

What Happens Over 30 Years?

The power of compounding becomes the defining factor.

-

The buydown saves interest steadily over time

-

The investment grows exponentially

By year 30, the difference becomes significant.

Projected Outcomes

-

Buydown Strategy: ~$1,000,000 equivalent financial impact

-

Investing Strategy: ~$1,450,000+ portfolio value

👉 That’s a difference of ~$450,000 in favor of investing

Why Investing Wins (Mathematically)

The key reason is simple:

Your mortgage interest is simple and declining… but your investments compound.

Mortgage Interest

-

Highest in early years

-

Decreases over time

-

Front-loaded cost

Investment Growth

-

Starts slower

-

Accelerates over time

-

Back-loaded gains

This creates a crossover point—typically around years 12–15—where investing pulls ahead and never looks back.

The Hidden Advantage of Liquidity

Another overlooked benefit of investing:

-

Your money remains accessible

-

It can be redirected, reinvested, or used in emergencies

-

A mortgage buydown is locked in and illiquid

Flexibility has real value—especially over decades.

When a Buydown Might Still Make Sense

To be fair, the buydown strategy isn’t wrong—it just serves a different goal.

A buydown may be better if:

-

You need lower monthly payments today

-

You are risk-averse

-

You don’t trust market returns

-

You plan to sell or refinance early

In shorter time horizons, the buydown can outperform.

The Big Picture

This isn’t just a math problem—it’s a strategy decision.

-

Buydown = Stability

-

Investing = Growth

But over a full 30-year horizon, history strongly favors compounding investments over interest savings.

Final Thought

If you can tolerate market fluctuations and think long-term, the numbers are clear:

The opportunity cost of a mortgage buydown is massive.

Instead of locking money into your loan, you may be better off letting it work for you in the market.

|

Dave Diegelman Broker Associate | License ID: 6799109-AB

|

Categories

- All Blogs (80)

- Buying a Home (18)

- Flipping (9)

- Home Improvement (1)

- Hurricane Utah (8)

- Landscaping (4)

- Market Report (35)

- NAR Settlement (3)

- National Parks (1)

- Notice of Default (1)

- Real Estate (59)

- Real Estate News (38)

- Rehab (3)

- Remodel (6)

- Retirement (11)

- Selling a Home (10)

- Staging (7)

- Towns (6)

Recent Posts